Many Swiss residents wish to acquire a second home in France, particularly in the Alps, on the coast, or in resort areas. This transaction, seemingly straightforward, quickly raises questions of estate law, real estate taxation, matrimonial regime, international succession, and rental management, especially when the property is occasionally rented.

This summary presents, in a legal and educational style, the main points of attention to secure the acquisition, optimize the structure, anticipate the resale, and avoid common mistakes between France and Switzerland.

Legal fundamentals before purchase: matrimonial regime and property ownership

Why the matrimonial regime must be analyzed as a priority

Before any acquisition, it is essential to identify the law applicable to the matrimonial regime of the spouses. The matrimonial regime determines who owns what within the couple and directly influences:

- the classification of the property as separate or community property

- each party’s rights in the event of separation or death

- the consistency of the ownership and transfer strategy

Practical impact on the acquisition

For example, if spouses married under a community property regime acquire a property using community funds, the property is intended to become part of the community estate. The deed of acquisition, the source of funds, and the classification of the property must therefore be consistent with the matrimonial situation.

Succession and second home in France: which law applies

Role of succession law

Succession law determines who inherits and in what proportions. For a couple residing in Switzerland, the succession is, in principle, connected to the last habitual residence or the last domicile of the deceased according to the applicable private international law rules, with an aim toward unity of succession.

Essential point: in a simplified approach, whether the property is acquired directly or through a civil structure, Swiss succession law is intended to govern the devolution of the property, subject to the mechanisms specific to private international law and any options available to the deceased.

Can another succession law be chosen

Changing succession law may be possible in certain cases, but it must be part of a coherent strategy and properly documented, in order to avoid creating a conflict of laws. In practice, the choice must also be coordinated with the matrimonial regime and the objectives of protecting the spouse and heirs.

Acquisition process in France: steps, notarial deed, and fees

Real estate acquisition in France follows a process generally structured around a preliminary agreement followed by an authentic deed signed before a notary. The choice of ownership structure may occur during the preparatory phase, between the preliminary agreement and the final signing.

In practical terms, the ownership structure is not intended to modify the course of the process, but it can profoundly transform the tax, succession, and resale consequences.

Choosing the acquisition structure: direct or civil real estate company

Why to avoid a commercial company for a second home

For the acquisition of a second home, the use of a commercial company is generally unsuitable. It increases complexity and cost without providing proportionate benefit. Several reasons frequently arise:

- the use of a foreign company does not guarantee anonymity, particularly due to reporting obligations and specific taxes

- the occupant may have to pay rent to the company, with tax and practical implications

- the taxation of the resale may be less favorable

- structure and compliance costs accumulate, especially in the case of a chain of companies

- adapting the structure after a legislative reform is often costly and burdensome

In practice, the analysis often focuses on two approaches: direct acquisition or acquisition through a civil real estate company, to be assessed according to family, succession, and tax objectives.

Income taxation: personal occupation and occasional rental

Personal occupation: no taxable income in France

An important point for Swiss residents: Switzerland recognizes the concept of imputed rental value for the occupation of a property one owns. This concept does not exist in French law: personal occupation of a property in France does not, in itself, generate taxable income in France.

On the Swiss side, the imputed rental value may still be taken into account for determining the applicable rate, according to the mechanism of exemption with progression.

Furnished rental: commercial classification under French law

If the property is rented, even occasionally, the situation changes. Under French law, furnished rental is fiscally classified as a commercial activity. Rental income is taxable in France under a regime that may be flat-rate or based on actual expenses, depending on the situation.

In the context of a second home rented occasionally, the flat-rate regime is often the one applied by default, while the regime based on actual expenses may be unsuitable when rental activity remains marginal.

In Switzerland, foreign real estate income may be exempt while influencing the tax rate applicable to other income, according to exemption with progression.

Rental via platform: caution regarding classification

Short-term rental via a seasonal rental platform triggers the application of the furnished rental regime in France. It is therefore necessary to anticipate reporting obligations, income classification, and potential impacts regarding social charges according to legislative developments and international coordination rules.

Real estate wealth tax in France: principle, thresholds, and Swiss comparison

Real estate property located in France falls within the scope of the real estate wealth tax when the net value of the household’s real estate assets exceeds certain thresholds provided by law. The structure of the French scale and its threshold effects require a prior quantitative analysis, particularly to avoid financing decisions made solely from the perspective of the French system.

On the Swiss side, real estate assets held abroad may be exempt from direct taxation while being taken into account for the rate, according to the principle of exemption with progression. The comparison must therefore be made comprehensively, taking into account the cantonal situation and the allocation of debts.

Financing through borrowing: deductibility of debts and cross-border effects

France: conditions for deductibility under the real estate wealth tax

In France, the deductibility of debts under the real estate wealth tax is regulated. Debts must notably be contracted to finance the acquisition, expenses related to this acquisition, or certain works, and meet temporal and traceability criteria. Refinancing a property initially acquired without borrowing may not produce the same effects.

Bullet loans are subject to specific rules: although they are not economically amortized, they may be fictitiously amortized for tax purposes, which progressively reduces the deductible base.

Switzerland: proportional allocation and debt dilution

In Switzerland, the treatment of debts depends on cantonal law and may lead to a proportional allocation of debts between assets located in Switzerland and those located abroad. This mechanism may reduce the expected benefit of borrowing intended to reduce French exposure, if the induced effect in Switzerland is unfavorable.

Methodological principle: avoid one-sided optimization

The decision to finance with cash or through borrowing must be based on a comparative analysis including:

- the value of the property and its position relative to French thresholds

- the impact on wealth tax according to the canton of residence

- the allocation of debts and effective deductibility

- wealth, succession, and liquidity objectives

A relevant strategy is a comprehensive strategy, which does not seek solely to reduce a tax in one country at the cost of an increase or added complexity in the other.

Resale: taxation of real estate capital gains

In the event of resale, the real estate capital gain realized on a property located in France is taxable in France, with allowance mechanisms linked to the holding period. On the Swiss side, the capital gain may be exempt according to applicable rules, subject to cantonal analysis and relevant treaty coordination.

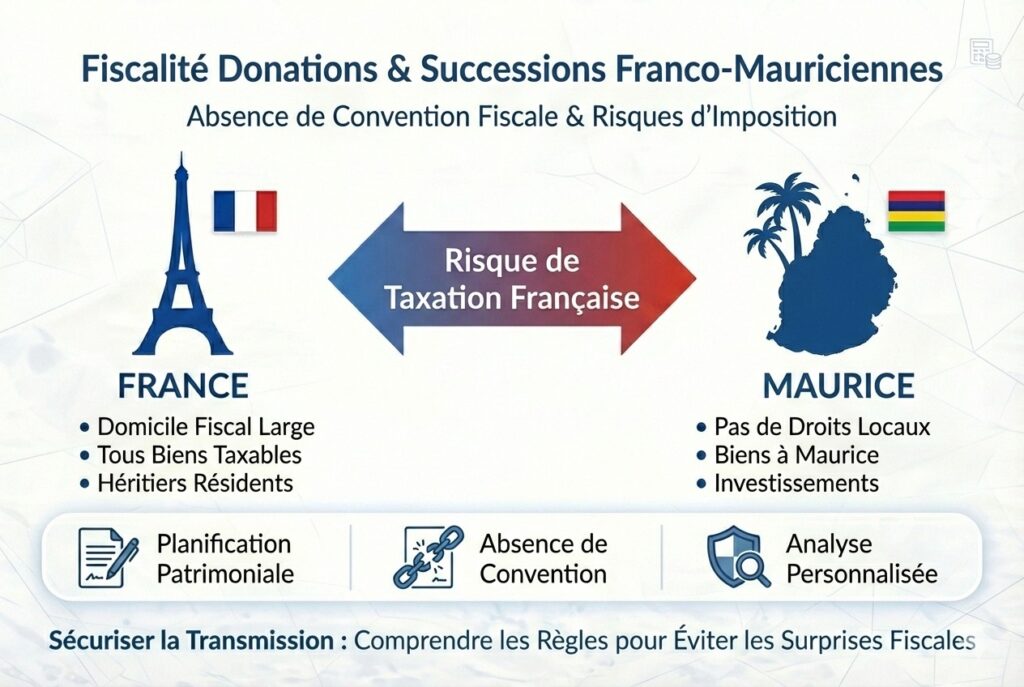

Gift and succession: absence of specific convention and jurisdiction of Swiss cantons

Regarding gift taxes and inheritance taxes, it is important to note the absence of a dedicated bilateral convention between France and Switzerland since the termination of the previous agreement. Each State therefore applies its own internal rules, and on the Swiss side, these taxes fall under cantonal fiscal sovereignty.

In practice, real estate located in France is taxable in France under gratuitous transfer taxes, while the treatment on the Swiss side will depend on the canton and the family relationship, often with no or low taxation in direct line in several cantons.

Debts and transfer: different treatment between succession and gift

In France, debts related to the acquisition of the property or certain works may, under conditions, be deducted from the inheritance tax base. Regarding gifts, the treatment is generally more restrictive, except for mechanisms of transfer of debt burden meeting strict conditions.

A practical point deserves to be considered: lending institutions in France frequently require borrower insurance, which may lead, in the event of death, to the repayment of the loan and therefore the disappearance of the deductible debt upon opening of the succession.

Conclusion: an integrated civil, tax, and succession approach

The acquisition of a second home in France by a Swiss resident requires a structured analysis of the interactions between matrimonial regime, succession law, ownership structure, furnished rental, real estate wealth tax, deductibility of debts, and gratuitous transfer taxes.

The key is to avoid decisions made in isolation. The right choice of ownership and financing depends on the balance between the French and Swiss systems, family objectives, and the transfer strategy. A preliminary wealth audit, coordinated with cross-border notarial and tax advice, remains the best way to secure the transaction and anticipate risks.