Wealth-related matters between France and Mauritius are common, particularly in the context of expatriation, real estate investment, or estate planning. However, the tax framework for gifts and inheritances is often poorly understood.

In the absence of a specific tax treaty between France and Mauritius covering gratuitous transfer duties, France may apply its domestic law rules, which can result in taxation in France even when the assets are located in Mauritius.

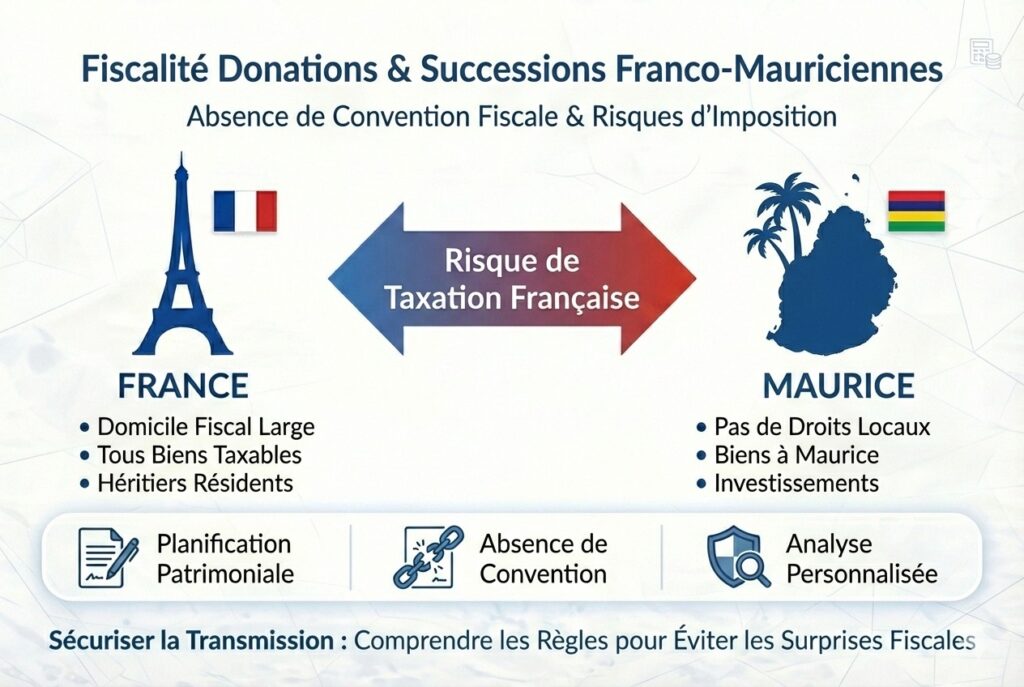

Absence of a Tax Treaty Between France and Mauritius

Gift and inheritance duties constitute a major issue in a Franco-Mauritian context. Indeed, there is no tax treaty between France and Mauritius covering these taxes. Under these circumstances, France may apply its domestic rules without limitation, both regarding the determination of tax residence and the scope of taxation.

Admittedly, there are no gratuitous transfer duties in Mauritius. However, this absence of local taxation does not provide protection against French rules, which may lead to taxation in France.

The Concept of Tax Residence Under French Tax Law

The concept of tax residence is decisive. According to Article 4 B of the General Tax Code, an individual is considered tax resident in France when they meet one of the following criteria, these criteria being alternative: a single criterion is sufficient.

Home or Principal Place of Stay in France

An individual may be considered resident in France if they have their home or principal place of stay there. Caution is required: if France is the country where you spend the most time, even if this represents fewer than one hundred and eighty-three days, the tax authorities may determine French tax residence.

Principal Professional Activity Carried Out in France

Carrying out a professional activity in France is an independent criterion. A simple corporate office, including an unremunerated one, may be regarded as a professional activity carried out in France.

Center of Economic Interests in France

The center of economic interests corresponds to the place where the taxpayer derives the majority of their income. All French-source income must be taken into account, including retirement pensions. If France provides your principal source of income, you may be considered tax resident in France.

It is therefore possible to be tax resident in France without being aware of it, sometimes even without ever setting foot on French territory. An individual may also be resident in France for gift and inheritance duty purposes while being considered a Mauritian resident for income tax purposes under a tax treaty.

Taxation Rules Applicable in France

With respect to gifts and inheritances, France provides for broad taxation based on the residence of the parties and the location of the assets.

- Duties are payable in France on all assets (movable or immovable), located in France, Mauritius, or elsewhere, if the donor or the deceased is tax resident in France at the time of the gift or death.

- Duties are payable in France on all assets received if the beneficiary (donee or heir) is tax resident in France at the time of the transfer and has been so for a significant period during the preceding years.

- Duties are payable in France on assets located in France, even if the donor, the deceased, and the beneficiaries are not resident in France.

Practical Illustrations

Example of an Estate with Economic Interests in France

A French national has lived in Mauritius for a long period and dies in Mauritius. He leaves real property located in Grand Baie, savings deposited in Switzerland, and an apartment in Paris. His principal source of income consists of his French pensions and rental income from the Parisian apartment.

In this case, the deceased may be considered to have his center of economic interests in France. He is therefore tax resident in France under French law, which results in taxation in France on all assets transferred, including those located in Mauritius and Switzerland.

Example of a Gift Taxable in France Due to the Beneficiary’s Residence

A French national living in Mauritius derives the majority of his income from investments in Mauritius and holds no assets in France. His only son has been tax resident in France since birth. He wishes to give him a villa located in Tamarin.

This gift may be taxable in France, not by reason of the location of the asset, but by reason of the tax residence of the donee in France at the time of the transfer.

Estate Planning Considerations

In a Franco-Mauritian context, several aspects must be anticipated in order to secure the transfer:

- The concept of tax residence of the parties is a key concept and must be analyzed with precision.

- It is advisable to anticipate the transfer in order to reduce its cost or, depending on the circumstances, avoid taxation in France.

- Trusts and foundations do not necessarily constitute tools for optimizing gratuitous transfer duties in France and may, in certain cases, increase the tax burden.

- In the absence of gratuitous transfer duties in Mauritius, there cannot be double taxation in the strict sense on these duties, but this does not prevent taxation in France.

Conclusion

The taxation of Franco-Mauritian gifts and inheritances rests on a central point: the absence of a specific tax treaty leaves France broad freedom to impose tax. An individual may be considered tax resident in France without being aware of it, which may result in taxation on assets located in Mauritius or elsewhere.

Before any transfer, a personalized analysis of tax residence, income, location of assets, and the situation of the beneficiaries is essential in order to secure the transaction and avoid significant tax consequences.